Friend,

This week, the House of Representatives passed H.R. 1628, the American Health Care Act, with my support. It is clear the Affordable Care Act is failing and must be fixed. Having reviewed the text of the bill and the Upton and MacArthur Amendments, I believe this legislation does what is necessary to protect individuals with pre-existing conditions, meets the principles for health care reform I laid out several months ago, and puts in place policies that will expand health care choices, increase access to care, and reduce costs.

This is the first step in a multi-step legislative and administrative process that will give individuals and families more control and choice over their health care decisions while increasing flexibility for states to deliver quality, affordable health care options to their residents.

I wanted to further explain my support of the bill by highlighting key parts of the American Health Care Act. Throughout the year, I conducted a Healthcare Listening Tour, where I heard from hospital administrators, doctors, nurses, patient advocates, people affected by the failing Affordable Care Act, and other stakeholders. These conversations reiterated how the failing Affordable Care Act is negatively affecting the constituents of the First District and furthered my resolve to work to make healthcare better for everyone. I remain committed to the constituents of the First District and will continue working to on behalf of their best interests.

The Case for the American Health Care Act

1. The Affordable Care Act (ACA) is failing

The Affordable Care Act promised to lower costs, increase access to care, and expand health care choices. It has failed on all three.

Costs: According to the Washington Post, “Insurers are raising the 2017 premiums for a popular and significant group of health plans sold through HealthCare.gov by an average of 25 percent, more than triple the increase for this year, according to new government figures. The spike in average rates for the 38 states that rely on the federal marketplace created under the Affordable Care Act was announced by federal health officials on Monday.”

Access: According to Bloomberg, “Failing insurers. Rising premiums. Financial losses. The deteriorating Obamacare market that the health insurance industry feared is here. As concerns about the survival of the Affordable Care Act’s markets intensify, the role of nonprofit “co-op” health insurers -- meant to broaden choices under the law -- has gained prominence. Most of the original 23 co-ops have failed, dumping more than 800,000 members back onto the ACA markets over the last two years.”

Choice: According to Time, “According to a new analysis from the nonpartisan Kaiser Family Foundation, almost a third of counties will have just one insurer participating in the exchanges by 2017, significantly more than the 7% of counties who had one option this year. That equates to 19% of all enrollees facing just one insurance option.”

And just recently we heard that Aetna was leaving the insurance exchanges in Virginia, meaning that Virginians in 50 of our 95 counties where Aetna operates will have one fewer insurance option. In 24 counties where it operates, there is just one other insurer selling Obamacare plans. This means Virginians have fewer choices and will face increased costs.

2. The Republicans plan to repeal the ACA will replace it with a bill that expands choice, increases access, and reduces costs

That plan is H.R. 1628, the American Health Care Act. The bill is the first step in a multi-step legislative and administrative process that will give individuals and families more control and choice over their health care decisions while increasing flexibility for states to deliver quality, affordable health care options to their residents.

The American Health Care Act repeals the ACA's individual and employer mandates and tax increases while phasing out the ACA’s health insurance subsidies and Medicaid expansion, replacing them with refundable tax credits and a more effective Medicaid funding model.

3. American Health Care Act Questions Answered

Will the AHCA kick 24 million people off of their health insurance?

No. AHCA will ensure everyone has access to affordable, quality health care, but not by forcing them to buy insurance or penalizing them if they don’t purchase insurance. Instead, the AHCA provides refundable tax credits to low and middle income individuals so they have an incentive to purchase insurance.

Moreover, the original Congressional Budget Office (CBO) estimate failed to take into account other planned legislative and administrative actions, which will help bring down costs and expand coverage. The CBO has a spotty track record when it comes to projecting health insurance coverage. When CBO originally scored Obamacare, they projected that 21 million Americans would have coverage in 2016. The reality was half that number, about 10.4 million gained coverage.

Our plan provides every American with access to affordable coverage. Low-income individuals not on Medicaid will receive a refundable tax credit to purchase insurance (meaning they get assistance even if they do not pay income tax). States can also further help low-income Americans through a new Patient and State Stability Fund.

I have a pre-existing condition. How does this bill affect me?

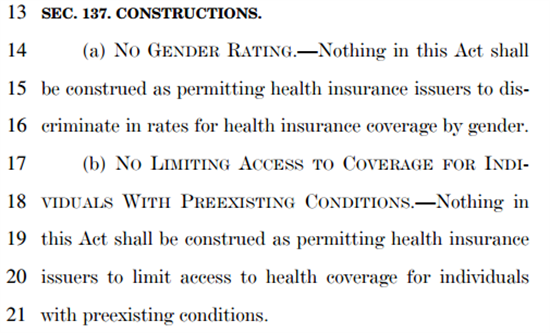

Under the AHCA, insurance companies cannot deny you coverage based on pre-existing conditions. And your health status cannot affect your premiums, unless your state asks for and receives a waiver—a condition of which is the state having other protections in place for those with pre-existing conditions. Even if your state does obtain a waiver, so long as you’ve been continuously covered, you still cannot be charged more. The bill provides added resources to help people in waiver states who have not been continuously covered to gain coverage. Bottom line, there are many levels of protection for those with pre-existing conditions in the legislation.

I heard about the MacArthur amendment allowing states to waive protections for pre-existing conditions. If this happens, will I lose all my benefits?

No. This amendment preserves protections for people with pre-existing conditions while giving states greater flexibility to lower premiums and stabilize the insurance market. To obtain a waiver, states will have to establish programs to serve people with pre-existing conditions. And no matter what, insurance companies cannot deny you coverage based on pre-existing conditions.

|

|

The MacArthur amendment only applies to the individual insurance market, where roughly 7 percent of the country purchase coverage. This means that the MacArthur amendment does NOT apply to 93 percent of Americans with employer-provided coverage or government coverage (Medicare, Medicaid, Tricare, VA benefits, and others).

Does the MacArthur amendment allow states to waive certain coverages, therefore raising costs?

Although it gives states an option to tailor coverage limitations, the process is very strict. A state must explain how a waiver will reach the goals of lowering premiums, increasing enrollment, stabilizing the market/premiums, and/or increasing choice. States must lay out the benefits they would provide. And most importantly, states may only apply for a waiver if they have their own risk pool in place. Again, the coverage of people with pre-existing conditions will be protected.

Even if a state asks for and is granted a waiver, no one’s premium may be priced based on health status if they have maintained continuous coverage. In addition to these protections, the AHCA provides significant resources at the federal and state level for risk-sharing programs that lower premiums for all people.

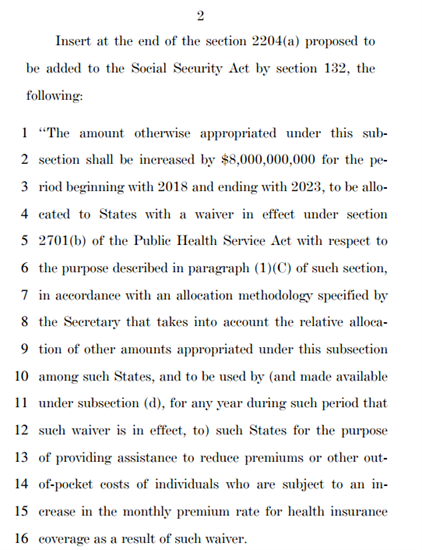

And what about the Upton amendment?

This $8 billion is on top of the $130 billion available to states through the AHCA’s Patient and State Stability Fund, which helps states repair their health markets damaged by Obamacare.

States can use the funds to:

- cut out-of-pocket costs, like premiums and deductibles

- promote access to preventive services, like getting an annual checkup, as well as dental and vision care

- promote participation in private health insurance or to increase the number of options available through the market

How will the AHCA affect seniors?

We know that seniors require and deserve more robust health insurance coverage. But under the ACA, the cost of the most generous plan for older Americans is limited to three times the cost of the least generous plan for younger Americans. Many health economists say the true cost of care is 4.8-to-one. So Section 135 of the American Health Care Act changes what is known as the "permissible age variation" to a five-to-one ratio in insurance premium rates so that seniors have coverage that works for them. Simply put, seniors will be able to purchase a plan that covers their true cost of care.

Are Members of Congress and their staff bound to the same rules as everyone else?

Yes. The House passed, with Rep. Wittman's support, H.R. 1292, a bill that ensures Members of Congress and their staff are treated the same way as everyone else under the American Health Care Act. What many people don’t know is that the Affordable Care Act included the exemption for Members of Congress and staff. Rep. Wittman opposed that language in the ACA, worked to get the exemption removed, and does not accept the stipend provided to Members of Congress under the Affordable Care Act to pay for his insurance premiums.

{kind=link}